India: scenarios for a sustainable development of the refrigeration sector

A recent study shows that an accelerated transition from HFCs to low-GWP refrigerants would allow India to go beyond the requirements of the Kigali Amendment and ensure sustainable growth of the refrigeration sector in line with soaring cooling needs.

Developing countries such as India, Brazil, China, and Indonesia are expected to drive global demand growth for refrigeration (including air conditioning). India currently has the largest unmet refrigeration demand in the world, but the low penetration rate of air conditioning - only 8% of Indian households currently have air conditioners - as well as other refrigeration equipment (cold chain, etc.) is not expected to persist. Projections suggest air conditioner sales will grow sixfold by 2038, with similar growth in other refrigeration equipment.

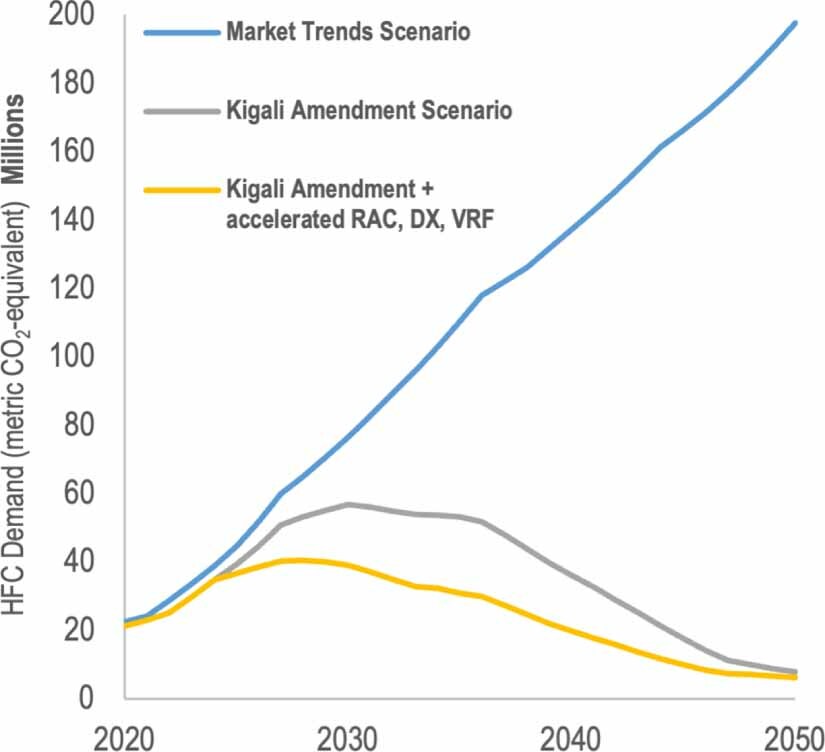

A recent article (1) presents three scenarios for India’s HFC demand until 2050. The first “Market Trends” scenario foresees no transitions from HFCs to lower-GWP substances beyond what has already begun. The two other scenarios are in line with the Kigali Amendment HFC phasedown schedule for Article 5 Parties and include a transition towards low-GWP refrigerants compliant with this amendment (second scenario) or accelerated with respect to it (third scenario). Thus, for stationary air conditioning, the transition from HFC-32 to HC-290 (propane) would take place in 2030 for the second scenario and in 2025 for the third scenario.

India’s current HFC demand is relatively low and amounts to about 23 Million Metric Tons CO2-equivalent (MMT CO2e) in terms of emissions. On a GWP-weighted basis, nearly two-thirds of this demand relates to stationary space conditioning and mobile air conditioning. The remaining third is split among chillers, small and large refrigeration, foam blowing agents, and cold chain.

- In the first “Market Trends” scenario, without Kigali Amendment implementation, results suggest that India’s annual HFC demand under current market trends could reach 76 MMT CO2e in 2030 and 197 MMT CO2e in 2050, from 23 MMT CO2e in 2020, without changes in the current mix of HFCs in use.

- The second scenario requires, in order to comply with the Kigali Amendment, that India freeze its HFC consumption in 2028 at a projected level of 59–65 MMT CO2e and phase down progressively over the following 29 years; in that case, annual Indian HFC demand would peak in 2030 at a projected 57 MMT CO2e and fall to 8 MMT CO2e by 2050. This trajectory would avoid cumulative HFC use of 2.2 GT CO2e through 2050 versus the current market trends without Kigali Amendment.

- If the third scenario is adopted, with actions taken to accelerate the refrigerant transition in particular in stationary air conditioning, India could peak its annual HFC demand by 2028 at 40 MMT CO2e and avoid additional cumulative HFC demand of 337 MMT CO2e between 2025 and 2050, exceeding its obligations under the Kigali Amendment.

The authors conclude that while measures are being prepared to implement the Kigali Amendment, including a national HFC phase-down strategy announced for 2023, the Indian government and industry have an opportunity to decide on strong actions that would take effect from the middle of this decade in order to avoid a potentially significant growth in demand for HFCs. This would allow the Indian refrigeration equipment market to continue to grow sustainably, in line with the country’s soaring refrigeration needs.

Source

(1) Hillbrand A. et al, Scenarios for future Indian HFC demand compared to the Kigali Amendment, Environmental Research Letters, Volume 17, Number 7, June 2022 https://doi.org/10.1088/1748-9326/ac7538